Honasa Consumer

Deep dive into the company which built MamaEarth

Hi.

Reading time: About 9 minutes

Disclaimer: I am a student analysing a company for my own purposes, in no way is this a recommendation to buy/sell the stock of the company. The post is only meant for informational purposes.

I’m trying something new this time. I thought it would be fun to write about a company that I did some work on. The company we will deep dive into is Honasa Consumer.

About the company

You might not know the name ‘Honasa Consumer’ but you might have heard of their brands like Mama Earth, The Derma co, Aqualogica, Dr Sheth’s or BBlunt . They have brands in the Beauty and Personal Care (BPC) segment. They are a digital first BPC company.

Industry

Global BPC market

Total market share for BPC products around the world expected to go from USD($) 646 billion in 2024 to USD($)736 billion in 2027. Expected to grow at a CAGR of 3.3%.

Indian BPC market

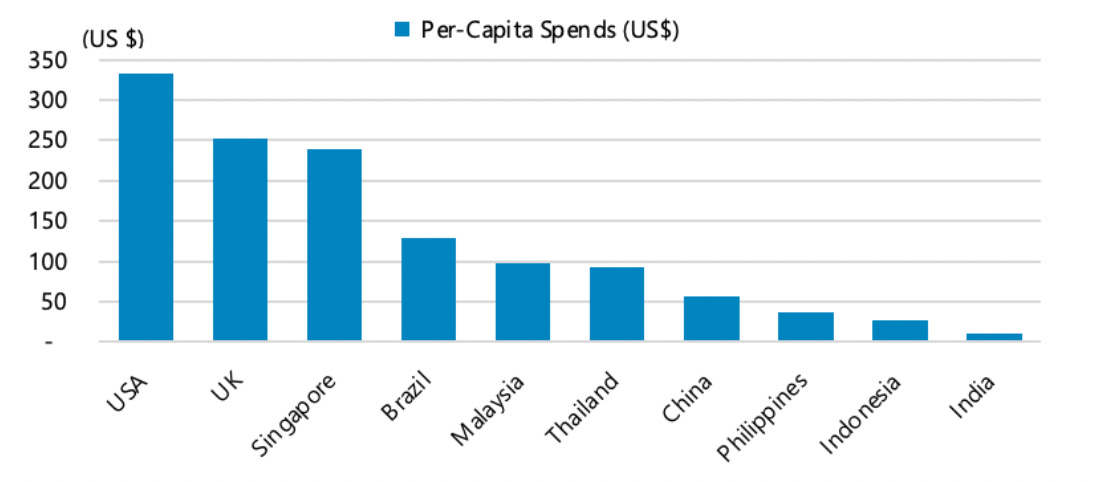

As a country India has lower per capita spends in comparison to peers in BPC. As the per capita income rises in India so will the BPC per capita spend. Indicating there is room for growth.

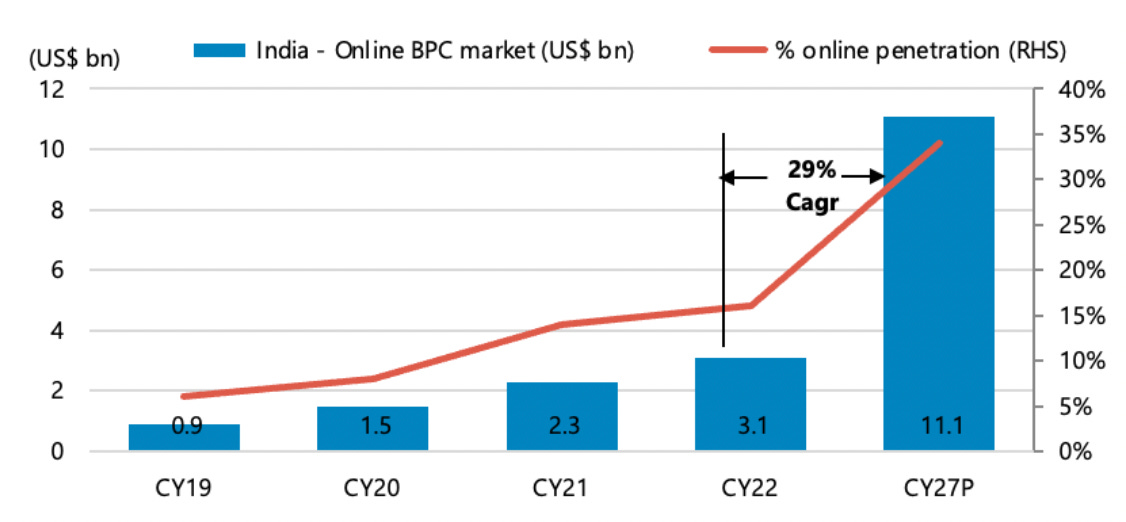

The Online penetration for India is expected to take off and with it the BPC online market. Expected to grow from 3.1billion to 11. At a 29% CAGR. This move is in favour of a company like Honasa consumer as they are a digital first BPC company.

Masstige segment to experience the most growth within the BPC segment by growing at 15% CAGR. Honasa Consumer targets the masstige segment which is also part of the entire mega trend of premiumization in India.

Fastest growing segments in the BPC market are Makeup ,Face Care, Bath and Body, Fragrance and Hair Care. Mama Earth operates significantly in the face care and hair care category as it makes up more than 60% of the revenues. Honasa has no products or brands which play the Oral care and wellness segment which are poised for single digit growth over the next few years

Business model

Innovation

Honasa has a team close to 50 people where Ghazal Alagh is the head of R&D.

Their innovation strategy is consumer centric. They pick up on the consumer trends that are going on in the world and also try and address the problems that they get to know about by speaking to consumers.

They recently acquired Cosmogenesis. It is an R&D firm which will help them formulate new products.

Innovation of new products contributes to approx 18% of the revenues (FY24). New Products have contributed ~9% to Q1FY25 Revenue from Operations.(1QFY25)

They keep picking up niches to play on. They picked consumers preferring home based DIY ingredient based products and active skin care early on. Their onion shampoo line has become a huge market. Their brand The Derma co. has done very well and has scaled well.

The biggest question that is unanswered is does Honasa have any edge when it comes to their R&D process? They have been able to pick these niches before others but is it something that can be repeated?

Manufacturing

Honasa Consumer outsources their manufacturing of products to contract manufacturers. This is the reason that they don’t have a lot of fixed assets and are more working capital heavy.

They have a deal with more than 30 contract manufacturers who manufacture their products.

They send their product formulations to these contract manufacturers and they conduct quality control checks at these facilities.

As they have scaled up significantly some of the contract manufacturers are exclusively making Honasa Consumer products.

Some of the contract manufacturers they have are Indo Herbal Products and VA Lifesciences LLP.

Outsourcing manufacturing has enabled them limited scale efficiencies but last quarter they had their highest gross margins of 71%.

Distribution

From a digital only company they started going offline with their main brand MamaEarth about 2 years ago. Most of the growth that is to be seen in the MamaEarth brand is coming from the offline channels.

Over the last few quarters the management has been very vocal on the change in their distribution from the super stockists to direct distributors. This will help them in their backend and inventory management. This is also the correct move to scale up further.

As of 1QFY25 their reach is ~2 lakh FMCG retail outlets. They are present in more than 3000 modern retail outlets reached and they are best sellers on e-commerce platforms.

The management has been very frugal when it comes to scaling their brands. They do not move offline for any of their brands unless they see significant demand for it offline. They have only recently started rolling out The Derma co. offline. It is in their culture to build brands online and then move offline.

Brand Building

Close to 35% of the revenues of Honasa go towards A&P. 2/3rds of this is towards digital advertising. (A&P cost includes channel spends on e-comm)

Most of their advertising spends go into their influencer marketing and their channel spends to push their products in e-commerce.

There is evidence in MamaEarth that as there is enough scale in a brand and enough awareness operating leverage kicks in and the advertising and promotion expenses reduce.

Each brand serves a different niche in the same segment but caters to different needs. They are capturing more market share in the BPC segment through this. (Mamaearth is toxin free, TDC is active skin care, Aqualogica is hydration for skin, Dr sheths is active bioskincare, BBlunt is professional hair care at home, etc.)

Advertising costs as a % of revenue is something which should be tracked. Last quarter surprisingly it went up. If their operating leverage in advertising does not kick in it becomes a big problem to look into. So this is one thing I would be tracking.

Growth levers

Offline distribution

Their move from super stockists to direct distributors is one which shows indication that there is demand for their products offline. As their move to distributors materialise they can control the supply chain better and know where their products are reaching and track it better through their backend systems.

Offline strategy for Mama Earth is to only serve the hero SKU’s instead of serving the long tail since they have limited SKU’s on display. If you go to a store to find MamaEarth products you will find their hero products only.(Vitamin c, Onion shampoo, Ubtan, etc.)

Younger brands

The younger brands in Honasa Consumer are the ones that are driving the growth for the company. The Derma co being the biggest of the four brands they have. They have crossed 500cr ARR for the derma co. and are projecting it to reach an ARR of 1000cr soon.

Subcategory of Active skin care is 2000cr ARR. TDC and Dr sheth have 33-35% market share.

Aqualogica and Dr Sheths expected to be 500cr ARR in next 3-5 years.

BBlunt has 4x since they acquired it and has reached an ARR of 100cr in Q1Fy25.

The company shut down one brand known as ‘Ayuga’. They failed to gain the traction or the product market fit and they are now sunsetting the brand.

Most of the growth in the company is going to come from these small niche brands scaling up.

Online company

The most intriguing thing about the company which has scaled up to 2,000 cr revenues in the last financial year is the fact that they started off online. The big brands like Ponds, Lakme, L’oreal, etc all launched offline. There is a big difference in the way they operate and the way Honasa consumer operates.

This difference of starting brands seeing if they work out or not and then scaling them up has a lot of advantages which can help set them apart from the traditional brands.

Offline distribution efficiency. Targeted store strategy : They can leverage their websites Pinched data to distribute products in areas where they see demand.

Faster launch of products. No hassle to launch new products online. Innovation enabler : A traditional FMCG company has to think about distribution and has a more complex task in releasing new products. Honasa just needs to make them available online and it is hassle free.

Digital ads: 2/3rds of ad-spend going digital drives the customers to the relevant online marketplaces.

Inherently also what the world has come to whether it is the west or it is India the rise of e-commerce has made it easy for companies to start brands which serve niches and solve problems which could not be solved before. A few of them work out to be even better sometimes than a niche. Onion shampoo or hair care is the example you look for. When they launched the product they did not know the market of onion hair care would become this big.

Key risks

Huge growth slowdown in MamaEarth due to size. Single digit growth in Mama Earth. (UVG grew in double digit)

Reliance on growth of younger brands. (Heavy reliance on them to do the heavy lifting as ME experiences growth slowdown)

Channel Check: Big brands have a lot of knowledge and acknowledged that they were caught by lethargy. They underestimated the niche brands growing big, now they will also work on it. So I think a wait and watch for a year or two where we can see how they fare will be the right thing to do. If the HUL, Marico, GCPL, etc cannot do what Honasa does then there is something there which needs to be looked at seriously.

Valuation

The median and average valuations of Indian companies indicates you would get Honasa at a huge premium to the other companies. (these numbers are dated from two months ago. FY24 numbers)

Conclusion

The company trades at a premium but it also has the best growth potential. The company going forward will grow their profits faster than their revenues due to their margin expansion plans. The way I see it is as of now the biggest question is still the business not the valuation. In a year or two we will get to know how the big brands fare against the brands like Honasa.

The management is solid I was really impressed by Varun Alagh and his capabilities. He worked in HUL, Diageo and Coke and is running Honasa very well.

I have not gone into the financials of the company but if you want to know please do reach out. My focus was on the business. If you have any insights or questions do comment below.

Thank you for reading,

Samvit.